When journalizing sales transactions in an intermediate accounting course, it is important to differentiate between the methods that the company is using. In this lesson, we will explore the net method versus the gross method for accounting for sales transactions. In this section, we illustrate the journal entry for the purchase discounts for both net method vs gross method. Net revenue (sometimes called net sales or net income) is the amount non resident alien filed tax through turbotax of money a company brings in after subtracting returns, discounts, price reductions, and other allowances and costs. This amount reflects the income you can expect to keep from your sales, so you have a more accurate view of how much the business is really earning and how much you have available to spend. For example, if a supplier offers terms of “2/10, net 30”, it means the buyer will get a 2% discount if they pay within 10 days.

Great! The Financial Professional Will Get Back To You Soon.

If the buyer pays within 10 days, the seller will record a debit to Cash for $891, a debit to Sales Discounts for $9, and a credit to Accounts Receivable for $900. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. Explore the principles, calculations, and financial impacts of net method accounting in this comprehensive guide.

Key Concepts of Net Method Accounting

If you’re a business owner, it’s essential to understand the difference between the net method and gross method of accounting for purchase discounts. However, both values are crucial to understanding what your company actively uses when making business decisions. Gross revenue shows sales ability, while net revenue reflects actual income after deductions. Together, they provide a complete picture for making smart decisions, managing costs, and ensuring long-term profitability. Using one without the other can lead to misinformed decisions when working to meet financial goals and grow the company. The main drawback to using the net method is that it does not record any information about the discounts taken or when they were taken.

Why understanding both metrics is crucial for business

This is because the amount of accounts payable that the company needs to make payment to the supplier under both methods is at the same amount. Net method of cash discount is the accounting method in which sales are accounted for assuming the cash discount will be availed by the customer. Sales under this method are thus not recorded at the full invoice value but at the reduced value after considering the effect of cash discount. If the customer doesn’t pay in time to receive the sales discount, you then record the sales discount in a separate account.

- Imagine that a business, “Gadget Store”, purchases 100 units of a product for $10 each.

- All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.

- This calculation can be more complex under the gross method due to the need to account for all sales and purchase transactions at their full value.

- After researching the various methods available and matching them up with your individual situation, you should better understand what will work best for your organization.

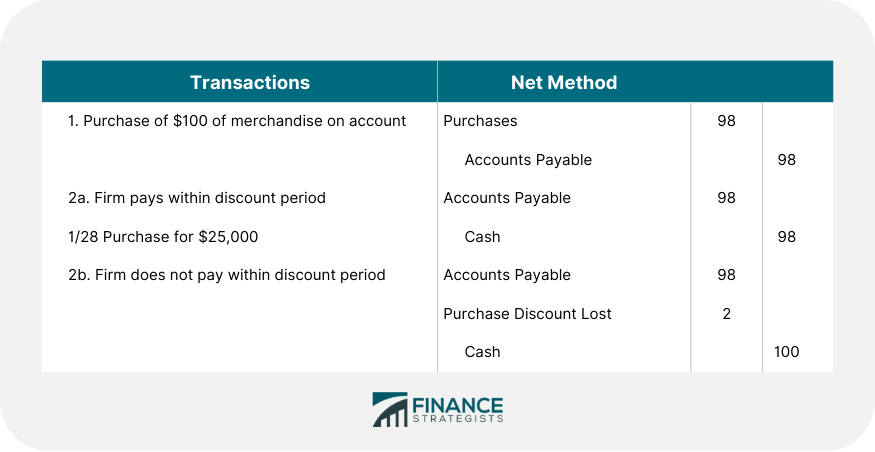

If you pay the bill within 10 days, you debit accounts payable for $500, credit cash for $490 and credit purchase discounts for $10 days. If you wait 30 days to pay the bill, you debit accounts payable for $500 and credit cash for the same amount. Credit helps promote business activity by allowing businesses and customers to pay for purchases some time after the sale. When employing the net method, calculating discounts becomes an integral part of the initial transaction recording.

How can you use gross and net revenue for financial planning?

However, it also suffers from the same criticism made against recording sales at the gross amount when discounts are offered. The F.O.B. point is normally understood to represent the place where ownership of goods transfers. Both methods give businesses the information they can use when making decisions on future purchases; knowing which type is right for a business depends on the company’s purchasing goals and needs. Businesses are always looking for ways to save money while still being able to serve their customers best.

The Gross Method results in a lower cost of goods sold figure, which can impact several places on your financial statements including net income and inventory valuation. It also helps to ensure that expenses accurately reflect payments made during a period. In order to illustrate precisely accounting for purchase discounts, let’s assume that ABC Co purchases merchandise inventory from its supplier on November 02, 20X1 at the original invoice amount of $1,500.

If you are on a personal connection, like at home, you can run an anti-virus scan on your device to make sure it is not infected with malware. Gross method accounting is a fundamental approach in financial reporting that significantly influences how companies present their revenue and expenses. This method, which contrasts with the net method, can affect various aspects of an organization’s financial statements and overall financial health. Explore the principles, impact, and comparisons of gross method accounting, and understand its effect on financial statements and revenue recognition.

The Gross Price Method, also known as the gross method, is an accounting approach used to record purchases and sales of inventory. At the time of sale, it is not known whether the customer will pay earlier and avail the discount. A question therefore arises whether to record the sale net of the discount offered, or alternatively to record the sale at full amount and account for the discount as a separate expense. If the business fails to take the discount, the entry to record the payment will be straight forward. The major difference between journalizing for sales using the gross method vs the net method is when the discount is recorded.

For example, if a company records a sale at its net value but later determines that the customer will not pay, it must write off the uncollectible amount. This adjustment ensures that the financial statements accurately reflect the company’s actual financial position. One of the primary advantages of the net method is its ability to streamline the accounting process.